By Bhanu Nallagonda, Cofounder, Ogha Technologies

March ‘26

The Age of Autonomy, The Infrastructure of Gigawatts and The Paradox of Intelligence

As the AI related voices and noise grew louder and louder, I felt it is pertinent to sit down, take a hard look at it and assimilate the progress so far and figure out where the things are headed, so that we can be where the puck is going to be and not where it has been or is currently. The key questions are the status of the frontier models, AI bubble, vibe coding and its impact, changes to the IT services landscape, threat to the jobs and the AX. The main objective is to scratch the surface and not be swayed by all the hype surrounding it. This blog is divided into multiple parts to make it an easier read. It provides an exhaustive, 360-degree analysis of the state of Artificial Intelligence as we speak. We will dissect the technical breakthroughs of the models, analyze the plummeting cost curves of inference, map the sprawling infrastructure of the AI arms race, explore the sociological shifts brought about by “vibe coding”, look at the strategies being adopted by the traditional IT industry to cope up with these transitions and assuage the investors’, students’ and the entry level developers’ anxiety. Finally, we will extrapolate these trends to figure out where it is all going, how it would reshape the industries, players and the startup eco system. All opinions expressed are personal. The pictures are generated by my co-founder, Kiran using AI tools apart from being a critique.

Introduction

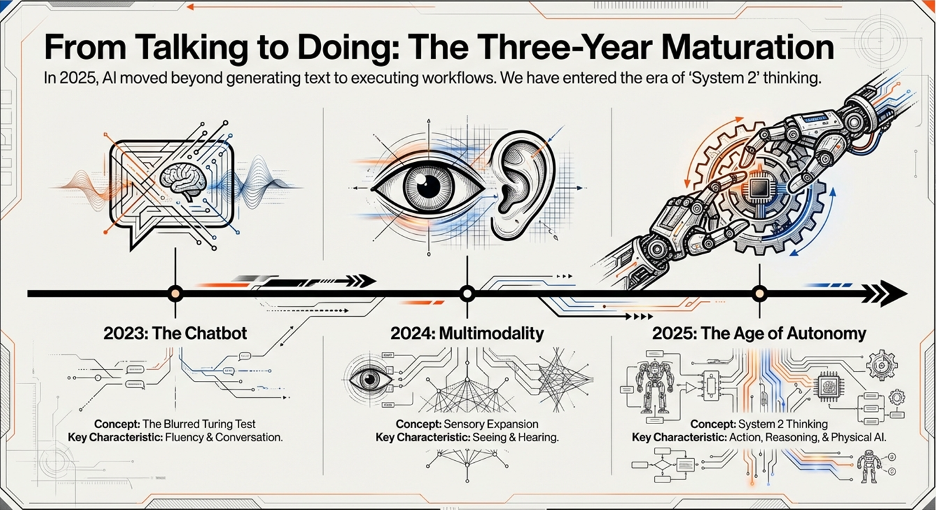

The year 2025 will perhaps go down in the history of computing as the year that saw AI’s fundamental maturation. 2023 saw the advent of the “Chatbot”, a kind of crossing the blurred line of Turing Test, but firmly, and following that 2024 was the year of “Multimodality” – where models learned to see and hear. 2025 has brought in the “Age of Autonomy”, the year when artificial intelligence started acting, beyond just talking. Physical AI and world models have started chalking out their own paths in the meanwhile.

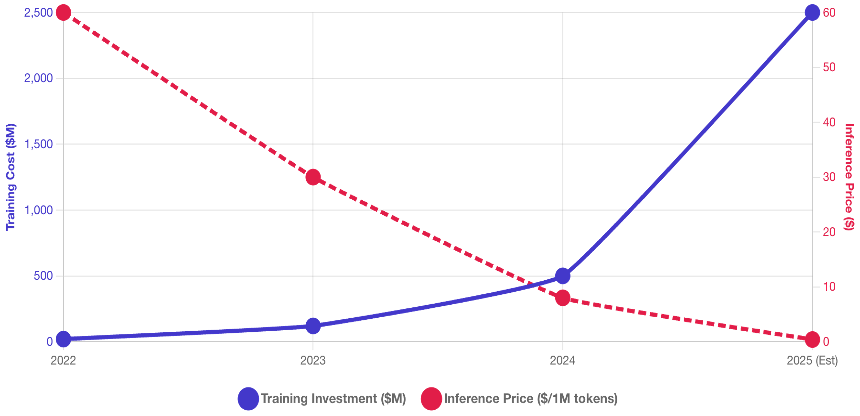

During the twelve-month cycle of 2025, the industry has navigated extreme contradictions. We have witnessed the raw intelligence of frontier models shattering benchmarks that were considered “impossible” merely a few months ago, with systems like Google’s Gemini 3 (and 3.1 Pro this year) and OpenAI’s GPT-5.2 (and 5.3 and 5.4 subsequently this year) demonstrating reasoning capabilities that rival human experts in narrow domains. Of course, the earlier benchmarks themselves got saturated paving way for new ones. More on it later. Simultaneously, the industry is grappling with a profound economic paradox: the unit cost of raw intelligence has plummeted by nearly three orders of magnitude, while the capital required to train a new model skyrocketed into billions and the aggregate cost of deploying enterprise AI also going up manyfold, driven by the voracious appetite of agentic workflows and “swarm” architectures. The paradox does not end there, many reports point now that more than 60% of AI system’s total lifecycle costs come from inference, not training! The share of inference would go up with increasing adoption, despite the cost of inference coming down and the cost of new models skyrocketing with predominant brute force approaches with an eye on AGI. It is also desirable that the usage goes up with real business benefits so that the huge investments made are paid back.

The physical manifestation of this digital revolution has become impossible to ignore. The race to Artificial General Intelligence (AGI) has morphed from a battle of algorithms into a battle of gigawatts. We are witnessing the construction of “giga-scale” infrastructure projects—like the $500 billion “Stargate” initiative and Meta’s “Prometheus” supercluster—that rival the industrial mobilizations of the 20th century. These are not merely data centres; they are modern cathedrals of compute, consuming energy on the scale of nation-states to power the next generation of synthetic cognition. However, a shadow looms over this expansive growth. A “circular economy” of funding has emerged, where chip makers invest in the very cloud providers that purchase their hardware, fuelling fears of a catastrophic asset bubble reminiscent of the dot-com crash. As valuations detach from current revenue realities, the market asks a critical question: is this the buildup to a new industrial revolution, or a prelude to a correction or even a crash?

Please read on Part I – The Model Landscape: The Frontier of Reasoning